Inside Ireland’s €150 Million Pension Deal with Tata Consultancy Services and the Launch of the Ireland-India Economic Advisory Panel — What It Means for 800,000 Workers

When we talk about scandals, most people think of backroom deals, padded expenses, or elected officials caught bending the rules. But sometimes the stories that shake public trust are hidden in the fine print of contracts and international agreements. That’s what’s happening right now in Ireland, where a decision about pensions — the very savings that hundreds of thousands of workers depend on for retirement — has sparked deep unease.

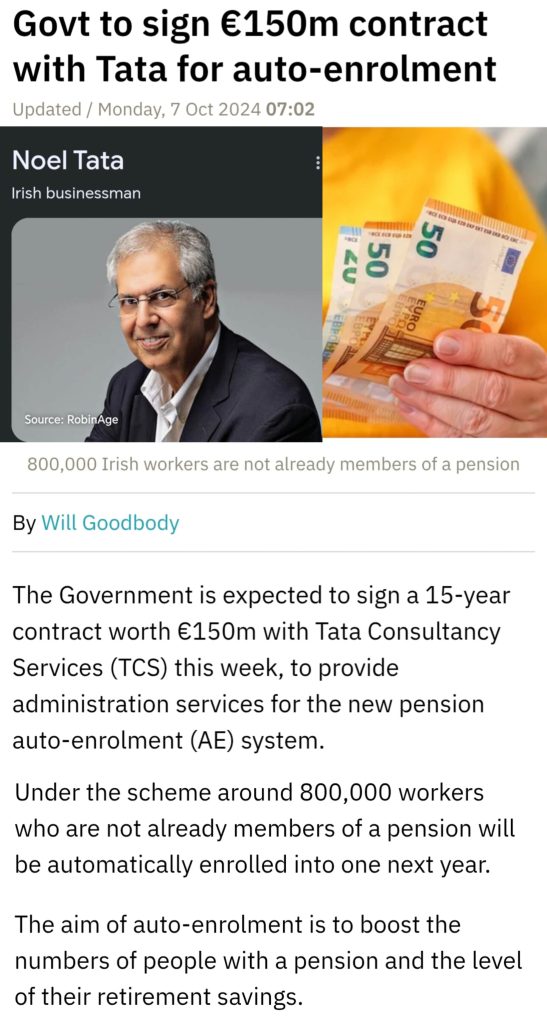

Earlier this year, the Irish government signed a contract worth roughly €150 million with Tata Consultancy Services (TCS), a global technology firm headquartered in Mumbai, India. The deal gives TCS the responsibility of designing, building, and running the new auto-enrolment pension system that is set to affect more than 800,000 Irish workers. On paper, this is part of a long-delayed effort to modernize Ireland’s retirement planning and make sure more people save for the future. But beneath the surface, many are asking questions.

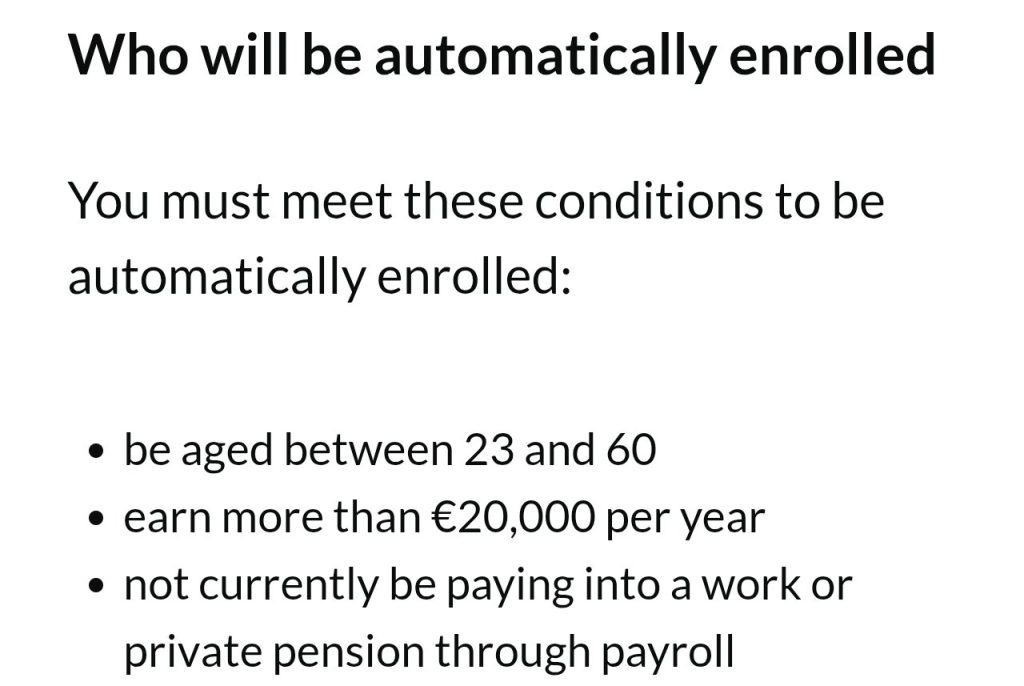

To understand why this matters so much, it helps to look at how pensions work in Ireland. For years, policymakers have worried that too few workers were saving enough for retirement. Without extra savings, people risk relying solely on the state pension, which may not be enough to cover the cost of living. That’s why the government committed to a national “auto-enrolment” scheme. Under the new rules, workers will automatically be enrolled in a pension plan unless they actively opt out. Contributions will be deducted from paychecks and topped up by employers and the state. It’s a big social shift, one that touches the lives of nearly every household in the country.

The government argues that hiring an experienced global firm like TCS makes sense. TCS is part of the Tata Group, India’s largest conglomerate, and has a strong reputation in technology services. It already operates in Ireland, with a delivery center in Letterkenny, County Donegal, employing hundreds of local staff. Officials say the company’s TCS BaNCS platform will provide the secure, reliable backbone needed to track contributions, manage accounts, and disburse funds when workers retire. In short, they believe outsourcing this work ensures the system is up and running on schedule.

But not everyone is convinced. Critics point out that a contract of this scale — set to last 10 to 15 years — effectively puts a cornerstone of Irish social policy in the hands of a foreign company. While global outsourcing is common in technology, pensions feel different. They are intimate, personal, tied to a sense of security in old age. People want to believe that their future isn’t being managed from halfway across the world, by executives who answer to shareholders rather than Irish citizens.

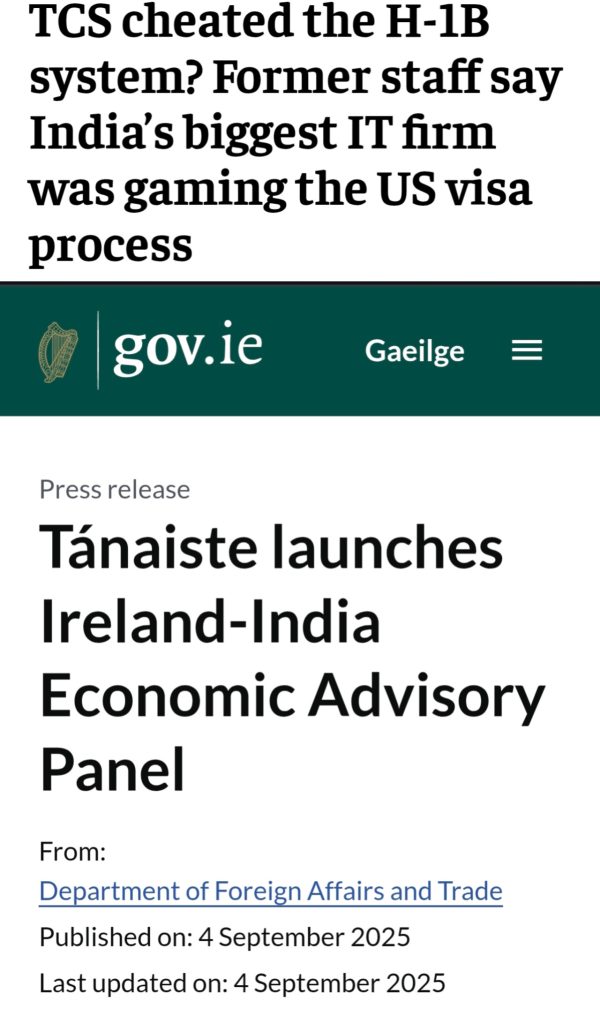

The timing of the announcement also raised eyebrows. Just days after the contract became public, Tánaiste Simon Harris unveiled the Ireland-India Economic Advisory Panel, a new initiative designed to strengthen trade and investment ties between the two countries. On the surface, this is a diplomatic move — Ireland wants to deepen connections with one of the fastest-growing economies in the world. India, for its part, sees Ireland as a bridge into the EU. Business leaders from both sides welcomed the initiative.

Still, for ordinary citizens, the overlap felt too close. The same week that a major Indian company was handed control of pensions, Ireland opened a new political and economic channel with Indian industry leaders. Whispers began to circulate: was this just smart international cooperation, or was Irish sovereignty being chipped away piece by piece?

It doesn’t help that Tata, like many multinational firms, has faced controversies abroad. Allegations of visa misuse and labor disputes have surfaced in the United States and Europe over the years, though none of these have been directly tied to the Irish deal. While TCS has consistently denied wrongdoing and continues to win contracts with governments around the world, the association alone fuels skepticism. Trust is fragile when it comes to pensions, and people tend to remember the warnings more than the reassurances.

The government has pushed back strongly against the critics. Officials stress that the Irish state will remain in control of pension policy. TCS is only providing the technological and administrative infrastructure. The Department of Social Protection will still set the rules, oversee operations, and ensure accountability. They emphasize that this is not a sell-off, but a partnership with a trusted global player that already has a footprint in Ireland.

And to be fair, there are practical reasons for choosing an outside contractor. Building such a system from scratch within the public sector could take years and cost even more. TCS has a track record of delivering similar platforms in other countries, and its existing base in Donegal allows for local oversight. Supporters argue that it’s better to use proven expertise than to risk delays and errors that could undermine confidence in the pension rollout.

But facts alone don’t settle feelings. For many Irish people, the worry is not about code or databases — it’s about control. There is an emotional weight to knowing that your retirement savings are tied up with a company whose headquarters are thousands of miles away. It adds another layer of distance between citizens and the state, and that distance can feel like a loss of sovereignty.

The debate also touches on something deeper: globalization and its trade-offs. Ireland has long benefited from foreign investment, especially in technology and pharmaceuticals. Multinationals employ hundreds of thousands of people and contribute heavily to the tax base. Yet each new deal raises the same question: at what point does reliance on global firms cross into dependence? Is it still a national pension system if the infrastructure is built and maintained abroad?

In moments like this, it’s easy for fear to take over. Some worry about data security, about sensitive financial information being processed by a foreign company. Others fear mission creep, imagining a day when outside business interests shape not just the delivery of services but the policies themselves. These are heavy questions, and they don’t have simple answers.

What is clear is that transparency will be crucial. The government must be open about how the contract is structured, what safeguards are in place, and how Irish oversight will work in practice. Independent audits should be published. Workers need to know not just that their money is safe, but that their voices still matter in decisions about their future.

As for the Ireland-India Economic Advisory Panel, it could very well prove to be a valuable bridge between two nations with much to gain from closer ties. But it will have to tread carefully to avoid the perception that it exists only to serve corporate interests. Democracy thrives on trust, and trust is fragile.

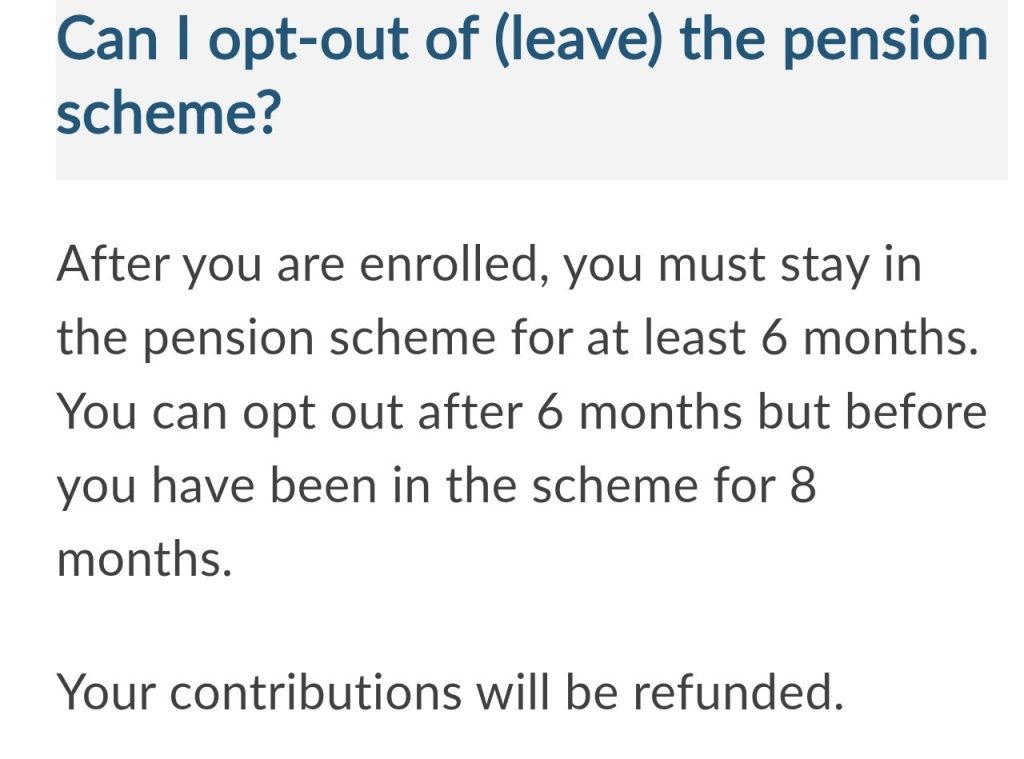

This story is still unfolding. In six months, when the auto-enrolment system kicks in, workers will have the option to opt out. Some may do so out of principle, unwilling to let a foreign company manage their money. Others will stay, hopeful that the system delivers the security it promises. Either way, the debate has already revealed something important: pensions aren’t just about numbers. They are about identity, sovereignty, and the social contract between citizens and their government.

Ireland’s leaders may see the TCS deal as just another example of international cooperation. But for the public, it feels far more personal. It is about who we trust with our future, and whether those decisions are truly being made in the interests of the people. That’s why this quiet contract has grown into something louder: not just a debate about pensions, but about what it means to be in control of our own destiny in a globalized world.